- 2,547

- 296

- Joined

- Mar 23, 2004

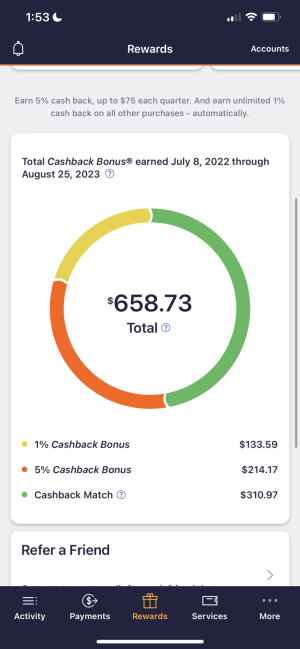

Finally got my Discover Double Cash Back bonus $500+ : hat

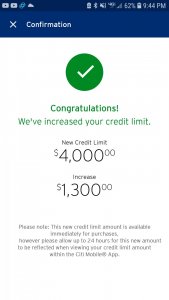

With credit cards I use them on a category basis. Depending on which one is in a bonus category I'll use. Discover and Amex have good discounts through their site too, like Nike is 15% off online. For more info on how to use credit cards to your advantage check out https://www.reddit.com/r/churning/

View media item 2261078

With credit cards I use them on a category basis. Depending on which one is in a bonus category I'll use. Discover and Amex have good discounts through their site too, like Nike is 15% off online. For more info on how to use credit cards to your advantage check out https://www.reddit.com/r/churning/

View media item 2261078

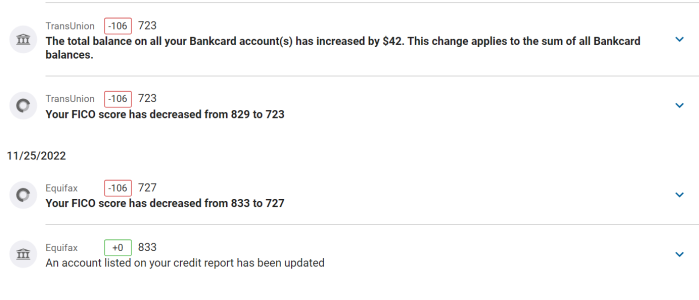

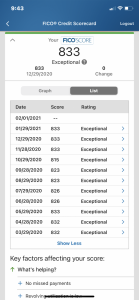

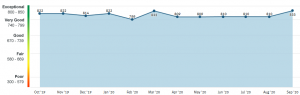

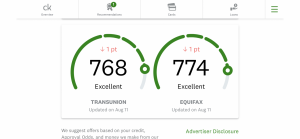

what kind of hard pulls have you had bro? Hard pulls are only like 5-10 points. Maybe your age of accounts will affect your score that much if you don't have many other credit lines that have been established for that long but a hard pull won't drop your score that much. And it only affects your score for one year, but it will show on your report for 2

what kind of hard pulls have you had bro? Hard pulls are only like 5-10 points. Maybe your age of accounts will affect your score that much if you don't have many other credit lines that have been established for that long but a hard pull won't drop your score that much. And it only affects your score for one year, but it will show on your report for 2