- 10,915

- 2,735

- Joined

- Apr 30, 2011

No. Pay in full before the due date and you're good.

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: this_feature_currently_requires_accessing_site_using_safari

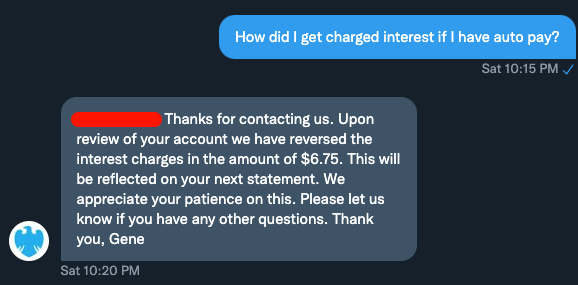

My statement cut on August 2nd, I made a large purchase on the 5th. My due date is the 2nd of September and it shows I owe 0.00 because that was my balance as of the 2nd. I have no issue paying it, but am moving end of month and would like more liquidity if possible.I think you'll be charged interest if you don't pay by the due date. Where does it say 0.00 due? Your statement or on your online activity or something?

My statement cut on August 2nd, I made a large purchase on the 5th. My due date is the 2nd of September and it shows I owe 0.00 because that was my balance as of the 2nd. I have no issue paying it, but am moving end of month and would like more liquidity if possible.

Like @Slighted said, they make a % of each transaction from the store. That's why some gas stations have a cash price and a CC price. Same with Arco stations. If you pay with cash, it's the face price and if you use a debit card they charge you 45 cents on the transaction.isn't that what the CC companies are in business for? we are using their money so there is a price to pay for that. I don't understand how they just lend money to people for free basically since some people have no yearly fees and such. I don't understand the credit card business completely just yet.Why let the CC companies make interest off of you?

You wanna pay more than what you already charged to your card?

and no, not pay more than what I charge, I mean pay the minimum or a little more each month. from what I read anything other than paying in full each month can sometimes be detrimental to your credit score.

I got an increase after 3 months. Will do it again in 6 months, rinse and repeat.So after 90 days for the first CLI with discover its fine to do every 30 days after?

^yup, good stuff. I know a lot of people dont realize that cash back/points/perks they get from their CC is coming from the merchants. I take advantage of it in almost all situations but for my kids daycare, I pay with a check because the owner is a friend/works her tail off, and i dont want to make her pay fees so I can get cash back. This one dad there who "brags" about being frugal was openly talking about using his CC to pay daycare for points, like he was wanting props. I was like dude youre making yourself look like a clown.

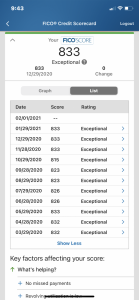

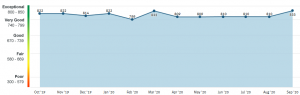

That's not the most ideal thing to do. Inquiries month after month will really impact your credit score in a negative way. Your credit limit isn't nearly as important as credit usage. Having a $2k-$3k credit card is more than enough. Having a high credit limit just to have a high credit limit isn't smart, nor does it improve your credit score.

But isn't that one of the perks of using credit cards? Isn't that why most of the people in this thread are pro credit cards? It seems to me you think the guy is a clown because the owner is a friend of yours...

That's not the most ideal thing to do. Inquiries month after month will really impact your credit score in a negative way. Your credit limit isn't nearly as important as credit usage. Having a $2k-$3k credit card is more than enough. Having a high credit limit just to have a high credit limit isn't smart, nor does it improve your credit score.

So after 90 days for the first CLI with discover its fine to do every 30 days after?

That's not the most ideal thing to do. Inquiries month after month will really impact your credit score in a negative way. Your credit limit isn't nearly as important as credit usage. Having a $2k-$3k credit card is more than enough. Having a high credit limit just to have a high credit limit isn't smart, nor does it improve your credit score.

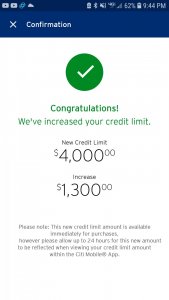

do they usually get back to you quick?

do they usually get back to you quick?Got the pending CLI from discover

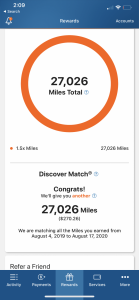

I have. Click the discover app and have your cart in another tab as well. Click the ebates button on Google chrome and activate.can you stack the discover 15% with ebates?

looks tough based on the fact you click to open shopping trips etc anyone had luck?