- 737

- 114

- Joined

- Jan 14, 2006

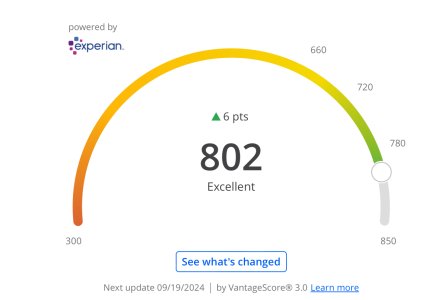

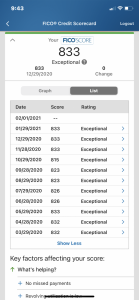

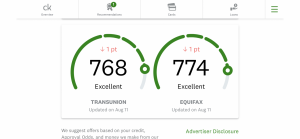

FYI, If you have a CC with NFCU, you can now check your FICO score online.

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: this_feature_currently_requires_accessing_site_using_safari

FYI, If you have a CC with NFCU, you can now check your FICO score online.

Anything higher than 740 will get you the same rate i believe no matter if you have 850.so i got a credit card this feb (my first credit card) and i just checked my credit score on the chase journey thing and my score is 738.

i read thats pretty good but is that good enough for like bigger things when buying a home, car, etc?

This, but remember CC credit score is not a mortgage credit score. Your mortgage score is usually much lower.Anything higher than 740 will get you the same rate i believe no matter if you have 850.

Not sure of the formula, but it depends on your income.

Also, everybody should stop worrying about credit limits and increases. If you get a CLI, cool. If not, move on. If you got your money right, utilization isn't an issue with your score so credit limits shouldn't matter. If you DON'T got your money right, you should focus your time and energy on paying your debts instead.

I think I already know the answer to this question

So let me preface it by saying that I'm joking, (90% joking)

So y'all know I'm gonna get a personal loan or whatever you call it to pay off my CC debt, then make payments to the loan... What if when I get that loan, I put it all down on the Roulette table (ONLY red or black, no numbers) and potentially double my bread so I can pay off the loan and the CC at the same time?

Not actually considering doing this, but it did cross my mind in a jovial manner.

But on a serious note... there's no legal, recommended way I can potentially double my money in a small period of time (to pay both the loan and the CC back at the same time), is there?

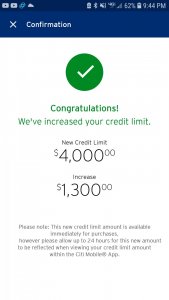

Just got another credit increase from discover. Credit limit is up to $34,500. I don't even use the card that much either.

What's your APR?

These offers are available 24/7 365, just go to the balance transfers section .Not too long ago they were offering another year of no interest or a lower overall APR for existing customers. Didn't pursue it bc I rarely use my card anyway.

On another note got a CLI on a card that I literally have never used. Thought the closed it already, not sure if I should cancel it & take the hit or keep it to preserve my score.

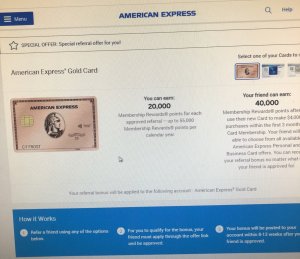

Annual Miles BoostSM for Platinum

The close of the calendar year is December 31, without regard to the time of the year that the account is opened. This means that for the first year of Card Membership, the Card Member's Eligible Purchases bonus period may be less than twelve months. If in any calendar year Eligible Purchases on the Platinum Delta SkyMiles Credit Card is $25,000 or more, the Basic Card Member will be awarded 10,000 bonus miles and 10,000 Medallion Qualification Miles ("MQMs" as defined in the Delta SkyMiles Membership Guide and Program Rules), and if in that same calendar year Eligible Purchases on the Platinum Delta SkyMiles Credit Card is $50,000 or more, the Basic Card Member will be awarded an additional 10,000 bonus miles and 10,000 MQMs. Eligible Purchases means purchases for goods and services minus returns and other credits. Eligible Purchases do NOT include fees, interest charges, balance transfers, cash advances, purchases of travelers' checks, purchases or reloading of prepaid cards, or purchases of other cash equivalents. Additional Card Member(s) are not eligible to receive miles through Miles Boost; however all Eligible Purchases by the Additional Card Member(s) will count towards the Basic Card Member's spend level to reach the Miles Boost threshold. Card Members may be permitted to have more than one Options, classic, Gold, or Platinum or Delta Reserve SkyMiles Credit Card from American Express account; however, Card Members are only eligible to receive one annual bonus for each type (i.e., Options, classic, Gold, Platinum or Reserve) of Delta SkyMiles Credit Card account from American Express.

To receive the MQMs, your account must be active, in good standing, and not in default at the time the MQMs are posted to your account.

thank you for the clarification herehttps://www262.americanexpress.com/...ymiles-credit-card/dal-805/dlp-terms#FeeTableAnnual Miles BoostSM for Platinum

The close of the calendar year is December 31, without regard to the time of the year that the account is opened. This means that for the first year of Card Membership, the Card Member's Eligible Purchases bonus period may be less than twelve months. If in any calendar year Eligible Purchases on the Platinum Delta SkyMiles Credit Card is $25,000 or more, the Basic Card Member will be awarded 10,000 bonus miles and 10,000 Medallion Qualification Miles ("MQMs" as defined in the Delta SkyMiles Membership Guide and Program Rules), and if in that same calendar year Eligible Purchases on the Platinum Delta SkyMiles Credit Card is $50,000 or more, the Basic Card Member will be awarded an additional 10,000 bonus miles and 10,000 MQMs. Eligible Purchases means purchases for goods and services minus returns and other credits. Eligible Purchases do NOT include fees, interest charges, balance transfers, cash advances, purchases of travelers' checks, purchases or reloading of prepaid cards, or purchases of other cash equivalents. Additional Card Member(s) are not eligible to receive miles through Miles Boost; however all Eligible Purchases by the Additional Card Member(s) will count towards the Basic Card Member's spend level to reach the Miles Boost threshold. Card Members may be permitted to have more than one Options, classic, Gold, or Platinum or Delta Reserve SkyMiles Credit Card from American Express account; however, Card Members are only eligible to receive one annual bonus for each type (i.e., Options, classic, Gold, Platinum or Reserve) of Delta SkyMiles Credit Card account from American Express.

To receive the MQMs, your account must be active, in good standing, and not in default at the time the MQMs are posted to your account.

Time to refi.

Anyone have recommendations on who to try?

Currently with BofA but have had rocket and chase send me prequalified letters.

What is your actual situation? Multiple credit cards totaling ~$20k in debt?That rejection email really has me feeling a type of way. What should I do? Best Egg? My credit report is fine other than my utilization rate which is what's really affecting that score

Idk what to do right now {

I thought this was America, people

What is your actual situation? Multiple credit cards totaling ~$20k in debt?

List out the cards / balance / interest rate

I'd pay off those 2 (Chase / CapOne) immediately if you can, especially since the CapOne is the highest interest rate.26k (rounded up amounts)

Amex 11,000 20%

Disc 11,000 23%

Chase 1,000 23%

Cap One 3,500 25%

I can/should/more than likely will have the cap one and chase paid off by beginning of August no problem.

Its a psych thing for me..seeing double digit balances really **** with my mental