- Apr 1, 2015

- 2,349

- 944

Just paid back my sisters for helping me pay for college. Almost debt free. Just another $8k remaining on my auto loan. Dont feel like paying it off yet since the interest rate is so low.

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: This feature may not be available in some browsers.

The problem with being rich is that it is relative. With our focus on single individuals, we’ll go ahead and outline a change in thought process as you inevitably move up *levels* in the game of life. We’ve always had the same belief regarding income and net worth multiples. The simple axiom is as follows:

“Double your net worth or your net income and your life changes”

You cannot start doubling from zero, but we’ll start there and walk through some of the changes you’ll see as you move through the ranks. (Key note: we do not include retirement savings in net worth, it counts as a zero)

Zero Net Worth: At this point most *future successful people* will have extremely high levels of will power. Will power actually declines as net worth and income go up because there is less reason to “sweat the small stuff”. Details become less relevant as earnings and net worth accelerate. Starting at zero? Everything matters.

A good way to think about net worth when a person has nothing? Constantly envious of what other people have. Any moderately competitive person is going to be unhappy during this time period as they see… every single day… that they are no where near their potential.

This is normal. Anyone in this stage is ready to do anything (and everything) to gain some traction and this includes insane time sucks such as working for a low hourly wage. Willing to trade time for money. There is no other immediate way to pay bills and start moving in the right direction.

A classic trap for the masses and most never figure a way out.

No time for fun because if a person has $0 to their name… they don’t deserve to have fun anyway.

$100K Net Worth: At around this point most people begin to feel some baseline level of security. Lots of effort (defined as hours worked in this rare instance) and money are at least *somewhat* correlated.

Anyone who reaches this modest level of net worth will know with certainty that anyone who claims hard work does not lead to more money (a minimal amount at least) is a complete liar and likely a failure at life as well.

Instead of doing anything for money, most in this camp will begin thinking in terms of “highest income per hour”. They haven’t escaped the trap yet. Instead they calculate how many dollars they are making per hour as that is their new way to free up time.

Generally, most of these guys find “quick hustles” to make a few hundred dollars here and there. They will be big on rewards credit cards and finding ways to get $100-200 sign up fees for opening up checking accounts.

Instead of using their valuable time to build a new skill they will usually invest free time in finding hustles for an extra $3-5K a year with all their extra time.

$200K Net Worth: Assuming a person successfully kept a decent job (typically a salaried employee), they begin falling into three categories at this point 1) frugality, 2) laziness and 3) scale. Right around this range most people have the ability to slack quite a bit. They will feel financially secure with a six figure bank account.

In Group 1, the person typically buys a home with the majority of the net worth as a down payment on a home. Then. Begins large and material cost cutting initiatives across the board. Minimal water bills, minimal spend on practically anything and moves towards home improvement (done by himself) to keep gaining momentum by essentially spending less… all cash flow goes to that mortgage.

In Group 2, a dangerous “YOLO” lifestyle is brought into play and the person sees his net worth stagnate to a rate of around $10-15K moves per year. Instead of trying to gain at rapid rates, he spends his time using his additional income because he doesn’t have a care in the world. This group is hit enormously during a recession and feels the real pain in their mid 30s as new skills were never developed.

In Group 3, a killer mentality usually comes out. This group sees that they are being used to make money for someone else. “No one is going to hire me unless they are making a profit off of me” is what they realize.

They are right. They find tangible skills to create a business as soon as possible.

$400K Net Worth: We’re down to two groups of people. People who picked up *event* driven income which we have talked about many times in the past (windfall earning typically due to ownership) or you have your frugality guys.

These two groups will never get along, although in some strange cases the windfall people also live frugal lives (they become disgustingly rich in the future). We’re in group one.

We have nothing but distaste for frugality type people as they have wasted their own valuable time. Instead of building something of value they spend time eating beans and rice. They are typically smart people and instead of using their brains to make hundreds of thousands of dollars more per year, they spend it finding ways to reduce their costs by tens of thousands per year. There is a floor to saving and no ceiling to earning. That is where the mentality changes.

$800K Net Worth: Generally, if a person has made it this far, there is no way they’re earning less than ~$200K per year (unless you’re old but as we stated your 401K does not count as net worth). The math simply doesn’t work.

If you were making $100K – $18K (retirement) – $22K for tax, healthcare, social security etc… You’ve only got about 60K per year and it would take almost twenty five long hard years to save to $800K (assumes 50% savings rate reinvested).

Your mentality is certainly not the same anymore. Your time is far too valuable to be wasted on low lifes and losers. At around this point, you’re becoming unattached with regular people and it is extremely difficult for anyone to believe you are who you say you are. The vast majority of people will believe you are a liar so you begin to *lie down* to skate under the radar.

You’ll find that most people are not happy for you and your tolerance for opinions that are not backed by actual success… declines at alarming rates. Good riddance to 80% of your smartphone contacts.

All You Care About is Scale at This Point.

$1.6M+ Net Worth: Most will go through one of the following: 1) drug addiction, 2) alcohol addiction, 3) family fall outs, 4) “friend” fall outs and 5) a complete disconnection with anyone their age. As a reminder, we are assuming you’ve been a single person this whole time (defined as no legal marriage) and we have no doubt at least one of the major issues listed above will happen. It is only a matter of time.

1) Drug addiction: Typically cocaine. This seems to be the general escape for most and it could lead to a long-standing downward spiral. Thousands of dollars per week spent on insane party habits.

2) Alcohol Addiction: Showing up to run your business reeking of booze… on a Tuesday morning. Typically leads to dropped balls for clients/customers… consistently… for a long period of time…. at least a year

3) Family Fallout: Quite common as well. No longer interested in any family member or group meet ups as it is not worth your time. Unhealthy belief that usually changes quickly (6 months or so) if your family has been good to you.

4) “Friend” Fall Out: Your list of contacts will shrink instantly in the 12 month period after reaching around $1.2M in net worth. Only a handful of people will be happy for you and of those people… most will be rich as well so they will understand everything that is happening as you transition to your new life.

5) Complete Disconnection: This likely contributes to all of the four items above. You won’t be able to have many friends your own age. Most will fall into one of these categories: 1) jealous, 2) think you are lying, 3) hoping you will fail. You can read it on their faces. You will tell them something basic about your life and they will then constantly question it later in time about 3-4 months in the future. They want to see if you’re a liar to highlight number three… Once you realize you’re being interviewed by someone who isn’t in your ball park you begin to despise them and cut them off forever.

Long-term? It is better for everyone.

Now that we’ve passed the “bad part” about getting to your first $1.6M or so, it’s interesting to note the change in thinking and how this will be a “tell” in the future if you’re speaking to someone who is well off. If you’ve made it to this level you’ll get to $2M pretty quickly but here’s the more important part when you’re around new people and want to know if they are rich.

The Tells

1) Doesn’t seem to care about who is around him/her. Meaning he/she is there to speak to one person usually and doesn’t care about anyone else in the group because in the back of his head he is thinking “I don’t have time for XXX”.

2) Not phased by brand name clothing, cars, celebrities, athletes or “job titles”. Sure some rich people are extremely insecure and are “all about that life” with high end brands etc. However. None of them will be phased by it. This means either the person will wear the nice brand without even mentioning it or they will wear items with no brands anywhere and not care. Subtle but important.

3) Generally more emotionless. Being emotional is a big burden if someone wants to get rich. Emotions are used to make money and if you have an enormous amount of emotion, it will be difficult to make tough un-emotional money making decisions. Reminder that all items are sold for pleasure or pain… emotions and feelings, nothing more.

4) Eccentric. This is broad, but if the person seems to be eccentric that is a dead giveaway that the person is either dead broke or extremely well off. You’ll be able to tell the difference when the check comes so it won’t take much longer than one hour to figure out.

5) Decisive. This has been proven over and over again. Wealthy people are generally decisive. They make a decision and move on living with the consequences. They do not prattle along with diatribes that go nowhere. They cut and move.

Now for the final obvious kicker as mentioned at the top… The only interest becomes scale.

Scale means the following: how much recurring benefit will I get over the next 10 years if I invest X time into doing this task. Once this philosophy sets in, it never changes.

Why would a person spend 1 year of effort to see a perpetual income stream of $10K a year, when one year of effort into another task would lead to $50K into perpetuity. Life becomes more about cash flow now and the future becomes irrelevant so rich people are constantly living in the present moment.

A person who is well off (our definition is never has to work if he/she doesn’t want to) then they have no interest in delayed cash flows. This is why floating and working capital metrics become more and more important over time.

Summary

At this point, we now realized all we’ve done is help gold diggers look for the signs of a successful person if they run into them at a high end bar. Oh well. But on a more serious note understanding the changes in belief systems is clear:

– At zero one believes any cent matters and will power is the only item they have to gain traction

– At around $100K they start looking for “high efficiency” time for money to have a personal life

– At around $200K most begin to relax and live that “yolo life”

– At around $400K you see a clear split between frugality and scale moves (scale always wins)

– At around $800K you become much more disconnected to society, uninterested in anyone who isn’t in the same league

– At $1.6M+ all you care about is scale, scale, scale and cash flow that you can use yourself

No, but I have a regular account. The only difference is that your gains grow tax deferred. It's the same as investing in bonds except these are backed by individuals instead of companies or municipalities.Anyone have a lending club IRA account ? Pros and cons ?

No, but I have a regular account. The only difference is that your gains grow tax deferred. It's the same as investing in bonds except these are backed by individuals instead of companies or municipalities.

My management fees are 30% of the gains.You should handle my finances.No, but I have a regular account. The only difference is that your gains grow tax deferred. It's the same as investing in bonds except these are backed by individuals instead of companies or municipalities.

Its nothing special but

^ Hook us up with the spreadsheet, fam.

I may blur the image and share show mine. It makes much more sense you can see it fleshed out and all the comments

^ Very nice. I've tweaked a few things for my own personal use and showed an example of what a fully fleshed out one might look like

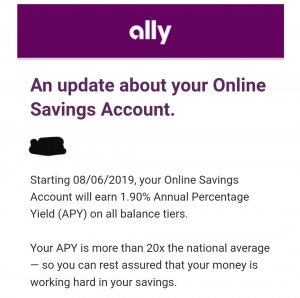

Safety and a higher interest rate. CD's are mostly preferred by older people who have saved a significant amount and don't want to expose it to too much risk. Typically they open several to "ladder" them based on when they will need the money and want a higher rate than a savings account.What are some of the general reasons for putting money into a CD? And benefits if any?

Interesting read:

Why is it that they dont include retirement savings in your net worth? What is it that they are including in net worth?

So I attempted to sign up for a gas card, and it said I couldn't because of an old delinquent account I had from years ago when I was 19 or so. I had a basic credit card with BOA and stopped paying it (I know, I know). Eventually the account disappeared. I scheduled a meeting tomorrow with them. I can still repair my credit right?

Saw this and thought of the thread. lol

http://www.businessinsider.com/i-en...e-my-fianc-refused-to-talk-about-money-2016-2