- 7,004

- 291

- Joined

- Jan 8, 2003

Lots of knowledge and contradicting info in here, just like all over the Internet.

for real man, I dont even know what to believe

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: this_feature_currently_requires_accessing_site_using_safari

Lots of knowledge and contradicting info in here, just like all over the Internet.

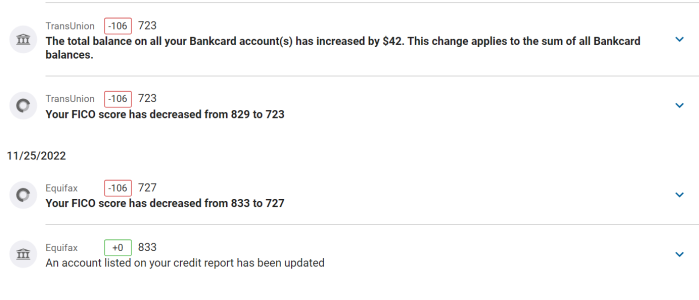

No he was right. You ant to try and keep like a 20-30% balance.

The system is not crooked, #2 is absolutely wrong, you should pay in full all the time, paying interest is ridiculous, why would you lose money? The debt has already been created when the transaction posted on your billing cycle, now you have the responsibility of paying back, the responsibility does not come from paying interest. #5 is not explained entirely. Yes the debt to credit ratio does exist, but it takes into consideration your entire credit ratio, so if you have 50K worth of credit and take credit card A to close to it's limit of 1000, it doesn't have a negative impact. If you're a creditor of course someone who has reached their limit across the board looks like a risky business venture. #1 is not necessary neither, the only time that comes into play is if you have two cards with chase, they factor your total credit limit with them when doing credit limit increases, so some people close one card to raise the total potential credit limit of another card. #4 and #6 should be explained more extensively as well. Rule of thumb is to ask for a credit limit after at least 6 months, most CC companies will honor the request if you have shown a good history with the card which makes sense. As far as credit inquiries is concerned many inquiries will lower your score but for me it's a negligible drop, and after a certain number it doesn't have any impact anymore, you can get the exact number from browsing MyFICO.com, I wouldn't push more than 3 every two years, the inquiries drop I believe after every 2 -3 years.

i have no idea why anyone would leave a balance on a CC unless it was 0% interest...i pay my statement balance every month

i have a 750+ credit score

Not necessarily. It's the best way to keep money in your pocket, which is the whole point in having a decent credit score in the first place.SO, paying it in full every month is the best way to raise your credit score?2. The only difference in your score would be not paying your balance in full and using too much of your available credit. If it's too high, it'll actually lower your score. Just pay the balance in full if you're going to use a credit card so you're not paying any more than you need to to the bank for a good score.

3. You have more of the bank's money available at your disposal to use.

its a forum with people obsessed with their credit

its a good forum with lots of info, lurked a lot times

They don't care how you pay it, as long as you do.

I have it setup through bank of america so it automatically pays my credit card with my $ from checking account. Will this build credit? (slowly?)

. It's all good cause I'm just going to use this card for gas and maybe my phone bill.

If anyone wants to apply for a Discover IT card then PM me, we both get $50

Helped Francox23 get one, we both got paid

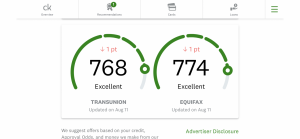

Ive been thinking about applying for this card, but im going to get my REAL credit score and credit report first. Credit Sesame says my score is 773 and they use the score from experian, credit karma says its 690 and they use trans union which it seems to be the one bureau that most places ignore..If anyone wants to apply for a Discover IT card then PM me, we both get $50

Helped Francox23 get one, we both got paid

I'm 26 and I have the following...

Capital One CC- Credit limit $3000

AMEX Blue Sky Rewards CC- Credit limit $3000

BestBuy (Citibank) CC- Credit limit $4000

Express CC- Credit limit $600

Got a little CC happy and got the first (3) in a 2 month span- NOT a good look and do NOT recommend.

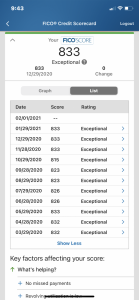

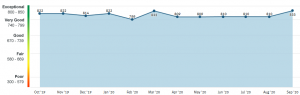

Regardless I have over a 700+ score and will agree with people in here, UTILIZATION is probably the most important part in credit cards. I have talked to finance majors several credit gurus read tons of forums and now a days 10% is what banks look for anything over that is considered negative.

I do got a question though for anyone that has knowledge on this...

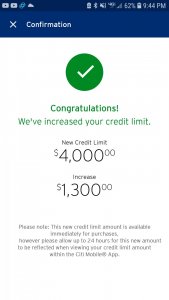

I want to request an increase on my AMEX and CAP1 cards its been over 2 months and never been late and always paid more then minimum. How much do I ask for? Do I ask for increases on both cards at the same time? Is there a limit that's too much to ask for? I'm looking for at least 8-9k on both, is that possible?

Would requesting an increase effect in any way getting a new auto loan? Or effect the APR on that loan?

Thanks!!

Ive been thinking about applying for this card, but im going to get my REAL credit score and credit report first. Credit Sesame says my score is 773 and they use the score from experian, credit karma says its 690 and they use trans union which it seems to be the one bureau that most places ignore..If anyone wants to apply for a Discover IT card then PM me, we both get $50

Helped Francox23 get one, we both got paid

Any reason why not the CAP1? It's hard using under 10 % utilization with a cap at $3000.amex- ask for $9,000. make sure you've had the account for at least 60 days. Thats what I did and got approved. Wouldnt try to get a limit increase with the cap 1 card.

amex- ask for $9,000. make sure you've had the account for at least 60 days. Thats what I did and got approved. Wouldnt try to get a limit increase with the cap 1 card.

Any reason why not the CAP1? It's hard using under 10 % utilization with a cap at $3000.

Would asking for increase effect my credit score at all or is it a soft pull?

Thanks

No, you'll want to pay it all off every month (otherwise paying interest defeats the point of a good credit score). You just don't want to use more than 10% in a given month.So I recently got my first credit card back around september or so and I've been reading through here. Good stuff. I just wanna make sure I understand this completely. So I hope someone can help me out.

-I have a limit of $1000

-lets say I spend around $400 for the month

So what you guys are saying is I'd want to pay off over $300 of that, like leave less than $100 left to still be paid. Then pay that left over amount on the due date?

Because if I pay it all off well before the due date it doesnt get reported?