antidope

Supporter

- 63,308

- 67,441

- Joined

- Jan 2, 2012

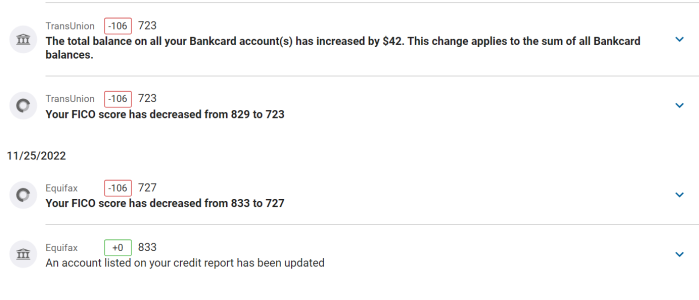

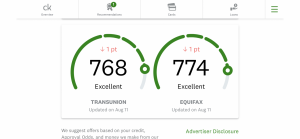

Thanks yo I appreciate it. My brother and I added each other as authorized users on each other's card and I wanna see how it affects me.@Anti- credit karma says they treat authorized users like your own

https://www.creditkarma.com/article/how-being-an-authorized-user-affects-credit